Alternative Fuels: Many Possibilities But a Clear Path is Evasive

“It was the best of times, it was somewhat confusing times, it was the age of wisdom, it was the age of the learning curve, it was the season of light, it was the season of, uh, still not enough light.” ― Deepest apologies to Charles Dickens, A Tale of Two Cities, 1859

As the world zeroes in on alternative energy sources and products that can deliver power and performance, there are advances that could sway even the most hardened skeptic. But challenges remain—tough challenges.

Two successes: renewable diesel and biodiesel

Renewable diesel (RD) is required now (since January 1, 2023) for all commercial harbor craft in California. RD is a drop-in replacement fuel for petroleum diesel. In California markets, RD is plentiful, and prices are competitive.

On the Great Lakes, the Canadian Steamship Line (CSL) has been using 100% biodiesel for the past five years. Its biggest complaint is price, not performance.

In California, manufacturers are cranking up RD production, ensuring plentiful supplies – and supply always impacts cost. The chemical and structural properties of renewable and petroleum diesel are similar, but they are different fuels.

Alt-fuels production is a labyrinthine story because developing, producing, transporting, storing and transferring new fuels is a mix of complex demands involving numerous industries. Alt-fuels have their own environmental impacts, particularly on agriculture and forestry. Ag-energy policies with alt-fuels are far from settled and present a tranche of issues which have to advance together. Success on one front does not mean that businesses can slide into a new normal, far from it.

Many parallel concerns

In anticipation of expanded alt-fuel usage, the U.S. Coast Guard’s (USCG) Office of Merchant Mariner Credentialing, on June 11 and 12, hosted a two-day meeting of the National Merchant Marine Personnel Advisory Committee (NMERPAC) Subcommittee on Task Statement 24: “Training and Experience Guidelines for Seafarers Employed Aboard Ships Using Alternative Fuels.”

The “Task Statement” for the Committee’s work specifically references IMO’s 2023 Strategy to “ensure an uptake of alternative and near-zero GHG fuels by 2030,” including methyl/ethyl alcohol, liquefied petroleum gas (LPG) and ammonia and hydrogen. Under a “Problem Statement” the Coast Guard writes that “seafarers need to be prepared to effectively take on their duties and responsibilities associated with these new fuels.” The USCG will use the Advisory Committee’s recommendations to develop national training guidance.

Methanol, for example, shows promise in alt-fuel work underway in California. It’s less energy dense than diesel but it’s a chemical that could replace diesel in slightly modified existing engines. Methanol has established safety protocols for existing industrial uses.

But for port operations, methanol raises numerous issues, from fires to atmospheric density. In April, the American Bureau of Shipping (ABS) published a document titled “Methanol Bunkering: Technical And Operational Advisory.” Note – advisory; regulations still needed. ABS presents a seven-page checklist of detailed tasks to maximize bunkering safety. As a chemical to be newly used as a fuel at the scale and extent of marine diesel, methanol presents a host of new and different issues, from worker safety to environmental justice. Again, progress on one front – engines and combustion – does not mean progress across all fronts.

Captain Ted Morley is a USCG Master Unlimited and Chief Executive Officer and School President of Maritime Professional Training based in Ft Lauderdale, Fla. Morley is Task Chair for the USCG’s alt-fuel safety advisory committee.

Capt. Ted Morley, CEO and School President, Maritime Professional Training (Credit: MPT)

Capt. Ted Morley, CEO and School President, Maritime Professional Training (Credit: MPT)

Morley said the committee will focus on the specific KUPs (knowledge, understanding and proficiency) needed by vessel crews. The committee’s work started with a review of current IGF (flash point) Codes and how they might need to be modified for alt-fuels. The committee will present recommendations for training to ensure that seafarers can “effectively operate within the (alt-fuel) environment and respond to and mitigate fuel-related incidents that could result in injury, death, shipboard damage or environmental pollution.” Initial recommendations will address alcohols, LPG and fuel cells. Future work will focus on batteries, ammonia and any additional proposed fuels.

Initial recommendations are due in the fall.

California: Driving the markets

When it comes to policies to make energy, California, with RD, is successful. In 2022, CARB officials forecast that commercial vessels would need approximately 55 million gallons of RD in 2023. Officials noted then that refineries were transitioning to RD, indicating enough product to meet new demands.

CARB officials were asked about that 2022 prediction, not just regarding fuel volumes but broader commitments to expansion. Lynda Lambert, a CARB spokesperson, said, yes, conversions and expansion have occurred. Refinery officials told CARB that RD production – both domestic and offshore – was projected to reach full capacity in early 2024.

As of mid-June, Lambert cited RD production at multiple operations, including:

- Phillips’ 66 Bay Area Rodeo facility: 30,000 barrels per day (about 460 million gallons) and on track to increase in Q2 to roughly 800 million gallons annually.

- A NESTE and Marathon joint venture in Martinez: projected to have 730 million gallons of capacity by the end of 2023; and,

- NESTE produced nearly 1 billion gallons annually as of late 2023 and expanded distribution in Northern and Southern California, partnering with NuStar and Vopak.

“The above numbers,” Lambert wrote, “show that the volume of renewable diesel being produced in California vastly exceeds (California’s) forecasted use.”

Max Rosenberg is California Port Engineer for Vane Brothers Company, the tug and barge company operating along the east and west coasts. Rosenberg was asked about Vane’s alt-fuel experience and the scale of those operations.

He said the company’s California fleet is running exclusively on RD, making the change in January 2023. “It’s been a relatively seamless transition for us,” he explained. “We haven’t experienced any performance issues that we could attribute to the fuel.” Vane’s team tracked a few initial minor problems with filters and algae, problems that resolved within a year.

Traditionally, RD is more expensive than fossil diesel. Rosenberg said, however, that “for the most part, despite inflation, we haven’t seen a significant increase in the price of (RD) fuel.” He suggested that federal and state tax incentives keep pump prices reasonable. “Otherwise,” he commented, “I think it’s fair to assume we would have seen a noticeable cost increase when we switched.” He said RD is plentiful in California because of industry focus but he added that may not be the case in other markets. “Without increased production elsewhere,” he commented, “I don’t believe global demand is being met.”

(© Christopher Boswell / Adobe Stock)

(© Christopher Boswell / Adobe Stock)

Success with biodiesel

Those comments match the experiences of Montreal-based Canadian Steamship Lines (CSL) which has been using biodiesel for five years. David Martin is CSL president and oversees alt-fuel issues. CSL uses FAME B100 biodiesel – “Fatty Acid Methyl Ester” – its chemical, building-block reference.

Martin said that “based on CSL’s extensive experience with FAME B100, no engine modifications are required, making it a viable drop-in fuel.” He said FAME is cheaper than RD but still more expensive than regular diesel. He noted that in both the U.S. and Canada federal funding intended to help lower costs is largely directed at producers, blenders and distributors. “There are currently no programs,” he pointed out, “to directly support end users, who have to contend with high prices and limited distribution. Programs aimed at end users would accelerate uptake of alternative fuels.”

Martin said biodiesel is an excellent option for meeting a fleet’s decarbonization targets. But he added that it needs to be part of a “broader strategy that considers geographic location, asset class, trade lanes, available fuels and shoreside storage constraints.”

“We have demonstrated that alt-fuels can work,” Martin stressed, but added that “governments must now step up to make (alt-fuels) a competitive option.”

MARAD’s upcoming California-based study

In 2022, the U.S. Department of Transportation’s Maritime Administration (MARAD) awarded a contract for a “a feasibility study on the future energy options for commercial harbor craft (CHC) operating in California.” It was due to be released in the second quarter of 2024, but is not yet available as of this writing (at the end of June).

MARAD wants a baseline ranking of “feasible and practical” potential alt-fuels and power options that (1) will reduce greenhouse gases (GHG) and (2) criteria pollutants (e.g., SOx, NOx and particulates) and (3) “can improve energy efficiency for harbor operations.” The timeline is through 2050.

Considering its scope, the study should answer a lot of questions:

“The study shall evaluate a variety of alternative fuels (methanol, ammonia, hydrogen) including biofuels (such as ethanol, bio-methane, bio-diesel, renewable diesel, FT-diesel) and power options as part of full-electric, hybrid propulsion, and power generation (such as shore power, solar photovoltaic, fuel cells, batteries). It shall also evaluate benefits and barriers of alternative fuels and power options and map the availability and implementation timeline (time projection) for these energy options through 2050. The time projection will be divided into short term (until 2030), medium term (2030-2040) and long term (2040-2050) and will be based on future trends. This study shall also describe the potential for these energy options to meet domestic environmental regulations.”

2030 is right around the corner. Likely, not every fuel and energy option will make the cut. MARAD’s advisory will help prioritize difficult decisions among many sectors.

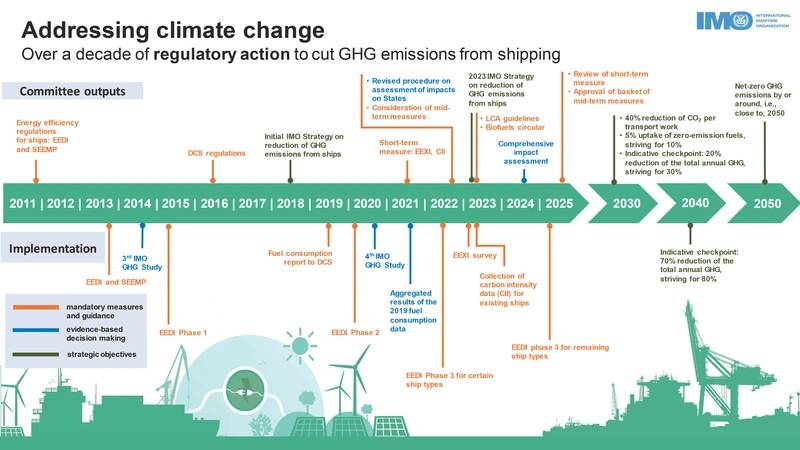

In 2023, the IMO’s Marine Environment Protection Committee (MEPC) presented a draft strategy and framework to cut GHGs from ships. At its recent March meeting, MEPC voted to adopt the framework but with enhanced targets. Net-zero is 2050 but commitments are due by 2030 to “ensure an update of alternative zero and near-zero GHG fuels, as well as indicative check-points.” MEPC’s timing will be close: it expects the 2023 Strategy will be finalized at the next Committee meeting in 2028 (see graphic timeline).

(Credit: IMO)

(Credit: IMO)

The IMO’s work focuses on international shipping, not exactly the same sector as inland waterways workboats and commercial harbor craft. Still, there are overlapping interests and concerns.

In comments on the 2023 Strategy the IMO presents the question: “Which new fuels will be needed?” Answers are vague. IMO writes that biofuels “could be one of the options” but it raises concerns with sustainable feedstocks and sustainable energy. It writes further that “there is room for all options to be considered, including electric and hybrid power, hydrogen and other fuel types.” It also mentions operational efficiencies, noting that just-in-time operations could prevent ships from waiting outside ports with their engines running, burning fuel.

From potential to kinetic…

Classification society DNV closely tracks and advises on alt-fuel developments. Considering all of the fuels that possibly could work in the marine sector, DNV was asked how these choices may be winnowed down? Maritime industry sectors and ports cannot build out production and logistics for every possible fuel.

“Collaboration is the fuel of the future.” - Jan Hagen Andersen, Business Development Director, DNV (Credit: DNV)

“Collaboration is the fuel of the future.” - Jan Hagen Andersen, Business Development Director, DNV (Credit: DNV)

Jan Hagen Andersen is Business Development Director for DNV. In an email reply Anderson wrote that biofuels (e.g., RD and biodiesel) will be important, but in the longer term, as supply scales up, there will be sustainability concerns both with feedstocks and production.

Andersen said, “It’s still early to have a strong position on the ‘fuel of the future’.” He added that “many parameters, beyond shipping, may affect this.” Andersen said that future maritime operators will select different fuels for different operations and sailings, depending on routing, vessels and commercial factors. “The wider uptake of low- and zero- carbon fuels will still take some time,” Andersen commented, “so continued energy efficiency improvements to reduce fuel consumption and to offset higher costs are critical.”

He said new alt-fuel supplies will advance in ways similar to how liquefied natural gas (LNG) advanced. He said new fuels will first appear at traditional bunker ports like Rotterdam and Singapore. In the U.S., hydrogen developments might push supplies of ammonia and methanol. Vessel and engine developments will require cross-sector collaboration. He cited DNV’s Fuel Path model as one example of a cross-functional analytical tool.

Andersen summarized - and advised: “Collaboration is the fuel of the future.”