Wheat Export Tariffs Likely to Slow Shipments from Russia

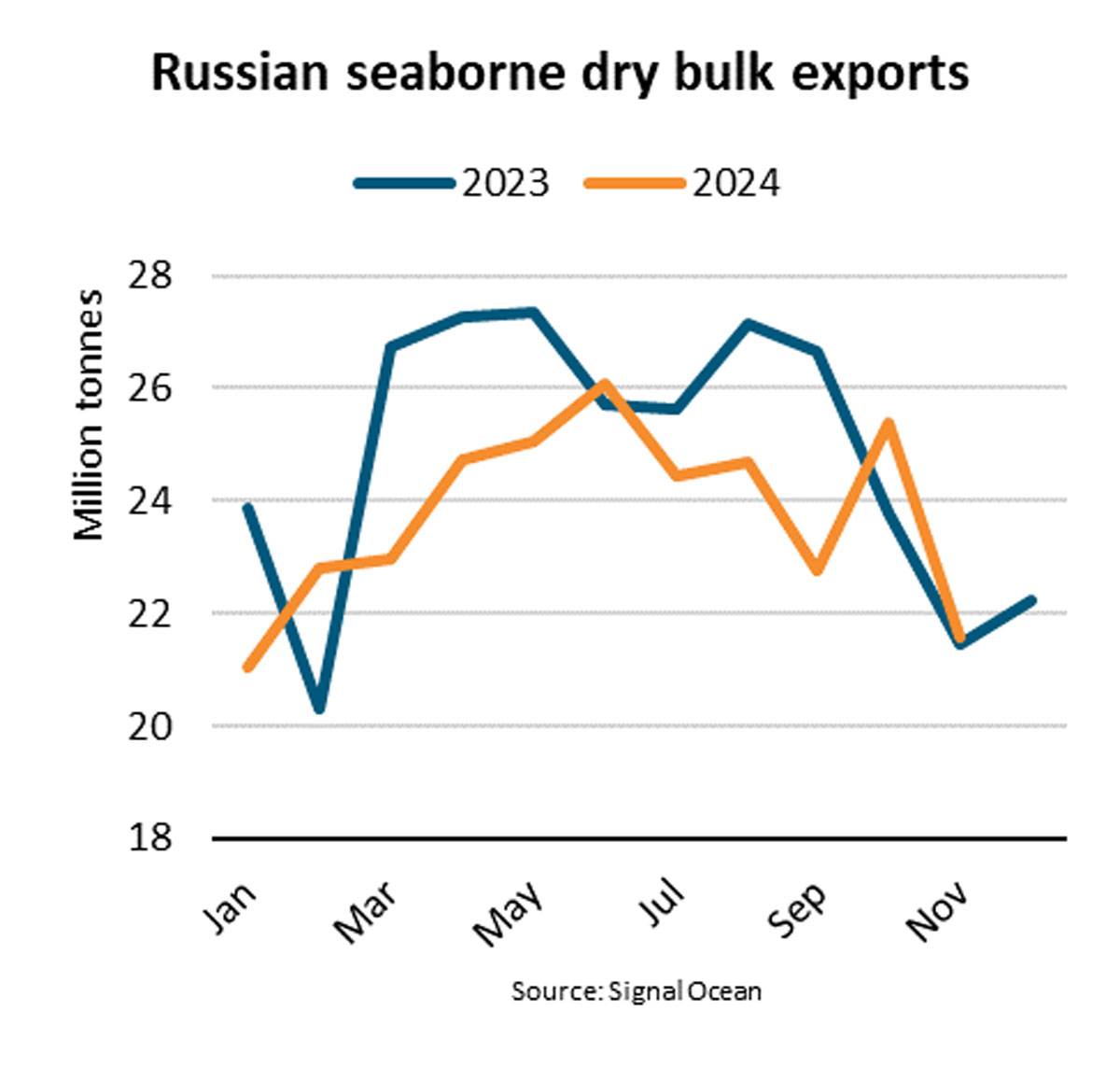

“Between January and November 2024, Russian seaborne dry bulk exports have decreased 5% y/y, driven by a 10% y/y decrease in coal shipments. The price competitiveness of Russian coal has deteriorated, compared to Mongolian, Indonesian and Australian cargoes, and a gradual increase in exports over land to China has also contributed to this decline,” says Filipe Gouveia, Shipping Analyst at BIMCO.

So far this year, wheat and fertilizer shipments from Russia rose 6% and 7% y/y respectively. After coal, they are the largest export commodities out of the country and therefore mitigated some of the losses from coal. Although this year’s wheat production fell by 11%, exports strengthened as inventories from the previous harvest were exported. Russian wheat shipments have grown considerably since 2022 due to large harvests in 2022 and 2023.

Soon, the price competitiveness of Russian coal will likely worsen further as Russian Railways increased their freight rates by 13.8% on 1 December. Sanctions have led to a spare parts shortage, making railway logistics more challenging and costly. As Russia relies on its railroads to transport coal to the ports, this directly affects export prices.

“Despite a notable decrease in cargo, the weaker Russian coal shipments have had minimal impact on the dry bulk market. Russian coal has been fully replaced by cargoes from more competitive exporters. Furthermore, sailing distances have not been impacted by this shift in suppliers,” says Gouveia.

In addition to a weak coal outlook, Russian wheat shipments may also decline soon. Russia has been facing significant food price inflation throughout 2024, reaching 9% in October. Bread prices are up 13%, likely influenced by declining wheat inventories amid a weaker harvest and stronger exports.

This has led the government to increase the wheat export tariff by 18% from 4 December and to implement a 62% smaller export quota between 15 February and 30 June 2025. Russia usually allows quota free wheat exports between July and January, following the wheat harvest in the summer, and then restricts them the rest of the year.

“Russian dry bulk shipments could continue to fall during the first half of 2025 as coal price competitiveness worsens and wheat volumes decrease. Unlike coal, a decrease in wheat shipments could have a more notable negative impact on the dry bulk market. Russia is the world’s largest wheat exporter, and as global inventories are low, other countries may not be able to fully replace the volumes,” says Gouveia.