Sleepy Week for Ship Recyclers

Even though the Indian sub-continent ship recycling markets have taken on a collection of smaller vessels of late, the week remains “sleepy” says cash buyer GMS.

Virtually no deals have been concluded, and this has put the squeeze on the global ship recycling sector.

“Dry bulk charter rates have been pushing on by the week as ship owners monetize the most from this sector. Containers and tankers too remain oddly off the recycling buffet, and this in turn is driving the ongoing dearth of viable candidates into overdrive, as chartering rates continue to hold through a time that many had been expecting them to falter with the turn of the year,” says GMS.

Small LDT units have seemingly taken the limelight of late, including several poor(er) condition Far East built / owned / operated units that remain less desired in light of their above-average weight-loss due to the poorer condition of their steel, says GMS.

On the ship-recycling markets front, Bangladesh continues to lead the way for another week, with Pakistan barely an arms-length behind. Yet, there have been a few indications that Gadani levels may be on the down in the coming weeks as local demand & L/C limits have been satisfied for the time being.

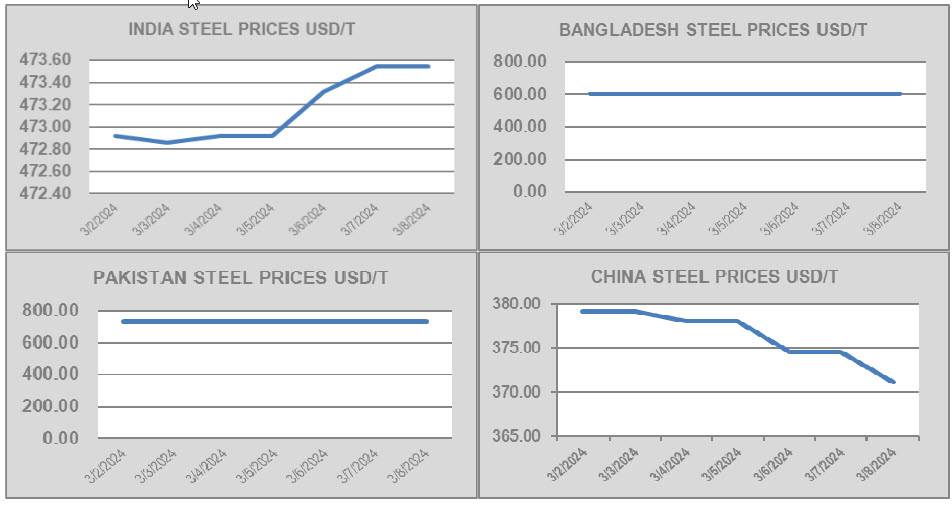

India also continues to struggle as Alang recyclers endure this prolonged downturn in their market and suffer through loss making deals just to acquire tonnage. Chinese steel is being offloaded despite strict anti-dumping measures being set in place. Therefore, it was a mixed overall week, with perhaps some trouble brewing on the horizon for the Indian and Turkish markets as their struggles show few signs of dissolving any time soon, and Bangladesh and Pakistan fail to get acquire any meaningful tonnage, despite demand & L/C limits being firm.

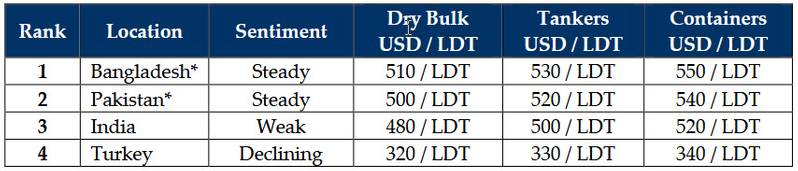

For week 10 of 2024, GMS demo rankings / pricing for the week are: