Preparing for IMO 2020: Marine Emission Solutions

Part I: Enhancing Engines & Fuels

"Wood Mackenzie forecasts a 25 percent increase in price for lower sulfur content fuel based on a SOx scrubber adoption rate of about two percent, but some scenarios could cause LSFO prices to spike by as much as 60 percent."

Around 80 percent of global trade is carried by sea. With more than 125,000 commercial and naval vessels operating around the world, ship-engine emissions are projected to rise by 250 percent by 2050 unless controls are imposed. Pollution from ship engines is so significant that in 2016 the International Maritime Organization (IMO) issued "IMO 2020 Rule" to cut fuel sulfur content 86 percent by the year 2020. A component of acid rain, sulfur oxide (SOx) emissions contribute to ocean acidification that harms marine habitats and ecosystems. To comply with IMO 2020, commercial vessel operators and owners have two routes to take:

1) Enhance engines and fuels: Commercial vessel operators can purchase higher cost low sulfur fuel oil (LSFO) or marine gasoil (MGO)—or for a high initial capital cost, they can retrofit their engine systems with scrubbers to remove SOx from emissions in conventional fuels.

2) Use alternative propulsion systems: Operators can convert to alternative propulsion systems, such as liquefied natural gas (LNG) or modern electric systems that adopt hybrid technologies which integrate energy storage.

To gain an understanding of the best course to follow, ship operators and owners are advised to consider how regulations will affect the cost and availability of LSFO, the value of using improved engines and fuels, and the value of employing hybrid/electric drive technologies as an alternative to a 100 percent fossil-fueled ship.

Regulations, fuel costs & availability

The IMO 2020 Rule requires ships to use MGO fuel with no more than 0.5 percent sulfur content compared to the current limit of 3.5 percent. In ships operating in Emission Control Areas (ECAs), which in North America extend 200 nautical miles from U.S. coasts, the sulfur content limit remains at the 2015 standard of 0.1 percent.

Sulfur and sulfur compounds naturally occur in petroleum, and special processing or low-sulfur feedstock is required to produce fuel with low sulfur content. Due to tight supplies and strong demand as the year 2020 draws near, there is no guarantee that LSFO supplies will be sufficient. To be confident in achieving the reduction from 3.5 percent to 0.5 percent, operators will need to do significant planning to ensure fuel is available for their vessel or fleet to avoid penalties.

Possible shortages could lead to significant price swings, making budgeting and investment scenarios complex. Industry analyst Wood Mackenzie forecasts a 25 percent increase in price for lower sulfur content fuel based on a SOx scrubber adoption rate of about two percent, but some scenarios could cause LSFO prices to spike by as much as 60 percent.

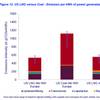

The possible price ranges are illustrated in Figure 1. The price premium per metric ton of fuel has averaged $225 between 2012 and 2017. As of October 1, 2018, the Houston bunker price was $465 for intermediate fuel oil (IFO380 = 3.5% sulfur) and $745 for marine gasoil (MGO = 0.5% sulfur), a price gap of $280.

In another scenario, an analysis by Stillwater Associates indicates that Rotterdam LSFO to high sulfur fuel oil (HSFO) spreads will increase from $2 in mid-2018 to $19 per barrel at the end of 2019, representing a percentage spread increase from 3 percent to 35 percent over 18 months, in anticipation of a sharp spike in demand for compliant fuel.

Foreseeing more complexity, analysts cited by Wood Mackenzie posit that the very low adoption rate of scrubbers used to remove SOx could lead fuel suppliers to jettison HSFO supply overall, disincentivizing further adoption of scrubbers.

Overall, these scenarios indicate the uncertainty surrounding LSFO prices and availability. If supply chains for the necessary quantities and types of fuel are not ready, global marine operations could be disrupted.

From a global perspective, Nordic standards and markets are the most progressive in moving to low sulfur MGO, as evidenced by rapid adoption of zero-emission technologies in several waterways. These developments serve as an example for how the rest of the world may respond.

Leading the way in North America, the Port of Long Beach (PLB) is targeting zero emissions by 2035. Starting now, substantial changes are already underway that will affect equipment purchases to meet emission standards. Other ports on the West Coast also have bold strategies, following the lead of PLB.

Fuel & engine improvements

When considering compliance with IMO 2020, most operators naturally think about adapting their vessels and engines to use whatever fuels may be available. Taking this track, ship owners have three options:

1.Use technology options that can utilize low-cost high sulphur fuel (HFO) with SOx scrubbers or exhaust gas cleaning systems (see discussion below)

2.Use available LSFO and MGO at higher variable cost, but which avoids capex investment for scrubbers or exhaust gas solutions

3.Use liquefied natural gas (LNG), a fuel that is virtually sulfur free. LNG prices are generally equivalent to or lower than HFO, but distribution facilities are not widespread due to limited demand today and high infrastructure development costs. As such, the extent of future LNG availability is questionable. Some ports are willing to invest, but LNG will not be available everywhere. Furthermore, the switch to LNG requires conversion to a different fuel management system that employs large refrigeration units to keep the gas in liquid state.

As an alternative to being exposed to the variable costs of LSFO, owners and operators can meet 2020 emission standards by investing in various technology options that can utilize HFO. For example, advanced marine engine designs are available that conform to the U.S. Environmental Protection Agency's Tier 4 engine standards. Tier 4 engines incorporate several advanced technologies—including selective catalytic reduction (SCR) and exhaust gas recirculation (EGR) (Figure 2). These two technologies significantly reduce nitrogen oxide (NOx) emissions for compliance in NOx Emission Control Areas such as the North Sea.

To achieve marine-engine emission reductions, engine manufacturers are employing several different approaches, such as:

1.Using modular exhaust after-treatment system (EAT) to meet Tier 4 for workboats, allowing flexible component placement for ship designers. An SCR system coated with vanadium is used for greater sulfur resistance, allowing the use of high sulfur diesel fuel.

2.Using Tier 4 SCR technology for lower fuel and urea consumption compared to Tier 3 engine types, while achieving high engine efficiency and emissions performance. Moreover, weight is 50 percent lower, full power acceleration is faster and engine performance is not derated if the SCR system fails.

3. Using engines ready for LNG in addition to electric and hybrid propulsion systems that incorporate analytics, automation and emissions control systems. (Using LNG and "hybrid" or low-sulfur -content fuels can also be done with Tier 3 engines to meet Emission Control Area requirements.)

4.Using a combination of all available technologies while promoting EGR as a way to use smaller SCR.

Emissions sensors are critical components used in engine exhaust systems to track and prove emissions compliance. One example of an in situ emission sensor technology is the marine emission sensor MES 1001 offered by Danfoss IXA. The MES 1001 ensures that fuel switching and systems are working by combining continuous emission monitoring and data collection for authorities. The sensors can also deliver data to control SCR urea dosage, improving resource utilization and system performance.

For vessel owners interested in reducing fossil fuel consumption, hybridization and electrification technologies complement or offer an effective alternative with many benefits. Look for Part II of this article in a the May 2019 “Green Marine” edition to learn more about the value of using alternative propulsion systems to meet IMO 2020.

The Authors

Jim Lerner is Vice President of Sales, Eastern US, for Danfoss Drives in Houston, Texas. His background includes 33 years in the electromechanical industry and four years in electrical/telecommunication technical engineering. He holds diplomas in business financials and marketing.

Jim Lerner is Vice President of Sales, Eastern US, for Danfoss Drives in Houston, Texas. His background includes 33 years in the electromechanical industry and four years in electrical/telecommunication technical engineering. He holds diplomas in business financials and marketing. Jon Holloway is the Head of Strategy for Danfoss Power Solutions, based in Hamburg, Germany. He was previously the Director of Strategic Marketing for Danfoss in North America, and has a background in finance, strategy, and marketing.

Jon Holloway is the Head of Strategy for Danfoss Power Solutions, based in Hamburg, Germany. He was previously the Director of Strategic Marketing for Danfoss in North America, and has a background in finance, strategy, and marketing.