Oil Product Tanker S&P Activity Down 45% -BIMCO

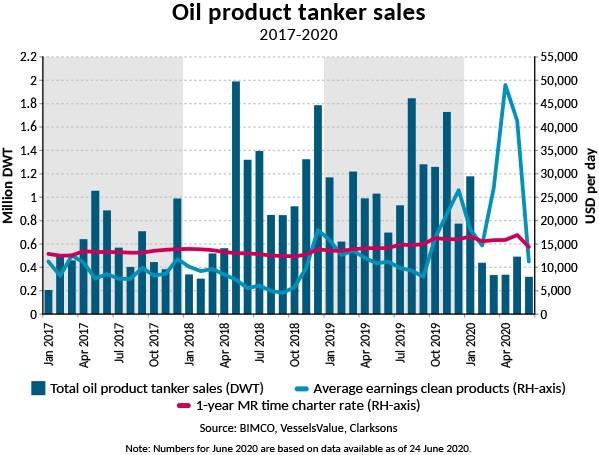

Oil product tankers earnings have skyrocketed in the first half of 2020, while the sale and purchase (S&P) activity of the oil product tanker market has slowed to the lowest level since 2016. Data from VesselsValue highlight that in the first five months of 2020, only 2.8 million deadweight tons (DWT) of oil product tankers have shifted hands in the second-hand market, a 45% drop compared to the same period last year.

A surprising S&P slowdown?

The oil product tanker market has thereby experienced a disconnect in the first half of 2020 with high spot earnings, while S&P activity has remained subdued.

However, S&P activity, as well as the 1-year time charter rate, often serve as better indicators for the strength of the underlying oil product tanker market. Although the oil product tanker S&P activity picked up slightly in May to 490,000 DWT from 330,000 in April, it is hardly a change in trend.

The low appetite for secondhand oil product tankers, despite spiking spot earnings, partly indicate that the medium-term outlook remains clouded by uncertainty. This is also indicated by the one-year time medium-range (MR) tanker charter rates that have started to feel the heat in June with substantial declines in a matter of weeks.

“Oil product tankers earnings skyrocketed way beyond break-even costs in April and May, in contrast to the muted S&P activity,” says BIMCO’s Chief Shipping Analyst, Peter Sand, adding, “The slow oil product tanker S&P activity can be attributed to oil product tanker owners holding on to their tonnage to tap into the extraordinary profits. Yet, it also seems likely that potential buyers were spooked by the challenges that lurked beyond the boom and held off on new acquisitions.”

Plunging oil demand gives dire outlook

The jury is still out as to which shape the recovery of the global economy will take. The International Monetary Fund (IMF) has recently placed their bets on a swoosh-shaped recovery with real global GDP forecast to decline by 4.9% in 2020 but grow 5.4% in 2021. BIMCO similarly expects the global economy to recover at a slow and gradual pace.

No matter the recovery shape of the global economy, annual oil demand is set to plunge in 2020. In June 2020, the International Energy Agency (IEA) forecast that oil demand for the full year of 2020 would decline by 8.1 million barrels per day. The worst drop in oil demand was seen in the second quarter, but demand will continue to be impaired in the coming months and negatively impact the prospects for oil product tankers in the second half of 2020.

Evidently, this bleak outlook has manifested itself in the S&P market. The low S&P activity in the first five months of 2020 stand in massive contrast to the two preceding years, where the S&P market was substantially more liquid. VesselsValue data highlights that S&P activity remained high through 2018 and 2019, with a total sales amounting to respectively 12.2 million and 13.5 million DWT, as the IMO 2020 Sulphur Cap deadline approached.

“Oil product tanker expectations had been set high for the IMO 2020 Sulphur Cap with shipowners contracting for new tonnage and buying up ships in S&P market, pushing up second-hand prices by 20-25% from 2018 to 2020,” Sand says.

“Some of these expectations were met, but for entirely different reasons than what was initially bet on. At the end of the day, it does not matter. Product tanker owners and operators have profited greatly in the first half of 2020 and hopefully bolstered their liquidity buffers for the murky waters that lie in the many months ahead,” says Sand.

2 out of 3 transactions had a European seller

Data by top 10 nations of buyers underscore that especially Asian and European buyers have shown greater appetite for oil product tankers. Chinese buyers accounted for 22.3% among the 10 largest buyers, while Greece and Denmark respectively accounted for 23.6% and 12.3%. Other large oil product tanker buyer nations in 2019 included Singapore, Indonesia, and United Arab Emirates.

The fragmented nature on the buyer side is not mirrored on the seller side, where Europe stands out as the dominating region, accounting for a whopping 67% of total sales by top 10 seller countries in 2019. As on the buyer side, Greece and Denmark stand out as the largest nations with respectively 28.1% and 19.8% shares of the top 10 seller countries. Singapore and Japan were the largest Asian seller nations in 2019 with 13.6% and 10.6% shares of total sales by the top 10 seller nations.

“European sellers have clearly dominated the oil product tanker S&P market in recent years, while the buyer side has been more fragmented. Greek shipowners are often viewed as competent asset-play investors and S&P data for the past couple of years, where prices had appreciated markedly, partly proves this point of view,” highlights Sand.

Oil product tanker asset prices down by 15.7%

Asset prices for oil product tankers have gradually recovered since 2017. As was the case with S&P activity, asset prices started to notably gain steam in the build-up to the 2020 IMO sulphur regulation coming into effect. This development is particularly evident with asset prices for MR oil product tankers, the workhorse of the segment, which peaked in the fall of 2019. At that time, a five-year old MR2, defined as 41,000-55,000 DWT, had appreciated to just above $30 million, a large improvement from the 2016 low of around $23 million.

However, prices have started to dip in 2020 with the second-hand price for a five-year old MR down by 15.7% year-to-date as of June 30 2020. Given the current oil demand forecasts which suggests a gradual recovery, it is likely that asset prices will continue to lose steam in the coming months.

However, asset prices are likely to settle at a price floor at some point, as the asset-play investors eye opportunities and enter the market. The asset-play strategy is essentially a game of patience and timing, where investors patiently wait for asset prices to depreciate and then strike when prices are perceived to be sufficiently low. The Global Financial Crisis in 2008 briefly plunged most of the shipping markets into the abyss, and in many cases cut asset prices in half, which allowed well-capitalized investors to strike.

The context of the economic crisis in 2020 differs greatly from that of 2008, but asset prices are similarly poised to depreciate significantly. In turn, the sharp depreciation of oil product tanker asset prices in 2020 will likely pave the way for a pick-up in S&P activity later in the year.

“Oil product tanker asset prices have generally appreciated in recent years on the back of expectations ahead of the IMO 2020 sulphur regulation. Now, with the demand shock of the COVID-19 pandemic, the tables have turned in favor of the buyers. Oil product tanker asset prices have come under substantial pressure and asset-play investors are now likely to emerge in the market,” Sand says.