BIMCO: Strong Bulk Market May Cool as 2025 Nears

The BIMCO Dry Bulk Shipping Market Overview & Outlook July 2024 by Niels Rasmussen, BIMCO’s Chief Shipping Analyst, anticipates that the supply/demand balance will strengthen in 2024 but weaken in 2025.

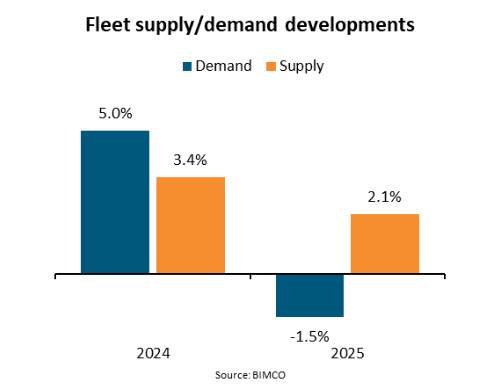

Supply is estimated to grow by 3-4% in 2024 and 1.5-2.5% in 2025, while demand is projected to grow by 4.5-5.5% in 2024 and weaken by 1-2% in 2025.

Freight rates are expected to stay strong during the rest of 2024, but demand could ease amid high inventories among importers. Freight rates are expected to weaken in 2025, should conditions in the Panama Canal normalize and the Red Sea conflict be resolved.

“We are now basing our forecasts on the assumption that ships will only return to the Red Sea in 2025 rather than during the second half of 2024. There are still no signs of a resolution to the conflict, and military interventions have not restored safety in the region. We have therefore revised our demand forecast upwards considerably for 2024 to account for the longer sailing distances resulting from rerouting via the Cape of Good Hope. Should the attacks in the Red Sea persist for longer than anticipated, then the dry bulk market will be stronger than forecast,” reports Rasmussen.

During the first half of 2024, the Baltic Dry Index remained firm amid strong demand. China continued to import high volumes of iron ore, coal and grains, and long distance sailings via the Cape of Good Hope increased as ships rerouted away from the Red Sea, just as they did from the Panama Canal. Consequently, tonne mile demand rose for segments smaller than capesize, supporting high freight rates.

The strong market boosted sale and purchase activity and pushed the value of five-year-old second hand assets close to newbuilding prices.

Capesize ships are expected to continue to perform strongly amid high demand and low fleet growth. Smaller segments may be negatively affected by weaker coal and grain shipments as well as higher fleet growth. These segments will be particularly affected by the expected end of disruptions in the Red Sea and in the Panama Canal.

Some demand risks persist in China. Slower than expected economic growth in the second quarter of 2024 highlights weak domestic demand.

Should China’s economy miss its 5% GDP growth target for 2024, the outlook for dry bulk demand will be worse than forecast. In addition, during the first half of 2024, China’s imports of iron ore and coal have exceeded demand and inventories have therefore risen sharply. A future correction of inventory levels could impact import volumes negatively.

Macro environment

The International Monetary Fund (IMF) forecasts the global economy to grow by 3.2% in 2024 and 3.3% in 2025, which is an upward revision of 0.1 percentage points for 2025. It has revised its growth forecast for emerging and developing economies up 0.1 percentage points for 2024 and 2025, due to stronger economic activity in Asia.

Inflation is expected to continue retreating over the forecast period. However, in advanced economies it is now expected to fall at a slower pace due to persistent inflation in services and high commodity prices. Consequently, interest rates may stay high for longer, which would slow down economic growth.

The Chinese economy is forecast by the IMF to grow by 5% in 2024, meeting the government’s target, and by 4.5% in 2025. However, the Chinese economy grew by only 4.7% y/y during the second quarter, raising concerns over whether the GDP target can be met.

India’s economy is forecast to grow the fastest out of all major economies – by 7% in 2024 and 6.5% in 2025. The IMF has highlighted strong domestic demand and private consumption, particularly in rural areas.

Demand

“We forecast dry bulk demand to grow by 4.5-5.5% in 2024 and to fall 1-2% in 2025. Cargo volumes are expected to grow by 1.5-2.5% in 2024 and by 0-1% in 2025. For 2024, we have revised our estimates up 1 percentage point due to stronger than expected iron ore shipments to China during the second quarter and a stronger outlook for coal shipments to India,” says Rasmussen.

“For 2025, we have reduced our estimate by 0.5 percentage points due to a weaker outlook for grain shipments. Average sailing distances are expected to lengthen 2.5-3.5% in 2024 but could shorten 1.5-2.5% in 2025. Distances are forecast to rise due to stronger cargo from the Atlantic Basin and increased sailings around the Cape of Good Hope instead of through the Red Sea and the Panama Canal. In 2025, sailing distances are expected to shorten, conditional on the end of the attacks in the Red Sea. Should attacks persist, demand would be higher than forecast.”

During the second quarter of 2024, conditions improved in the Panama Canal, as cargo transits rose 40.5% q/q, although they are still down 54.4% y/y. Meanwhile, cargo transits through the Suez Canal fell 22.4% q/q and attacks have not subsided despite military intervention.

The dry bulk orderbook stands at 95.9 million dwt, equal to 9.4% of the current fleet, only half of which is expected to be delivered before 2026. During the first half of 2024, newbuilding contracting slowed down 34.2% y/y.

Ship recycling is estimated to reach 4.4 and 7.2 million DWT in 2024 and 2025 respectively. “We have lowered our recycling estimates since our last update due to stronger than expected cargo volumes in 2024 and the assumption that Red Sea reroutings could now impact all of 2024. Nonetheless, we still expect recycling to gradually increase from the start of 2025, as the market’s strength wanes.”

Sailing speeds are expected to remain stable in 2024 but could fall by 0-1% in 2025. Since 2021, sailing speeds have gradually decreased, but so far in 2024, high freight rates have kept them from falling further. In 2025, we expect that they could marginally decrease as freight rates may cool and climate regulations continue to incentivise low sailing speed.

“We expect that a reduction in congestion could lead to a 0-1% y/y increase in supply in 2024. Ship capacity in congestion fell primarily in the capesize and panamax segments, in Australia and Brazil respectively.”