Key Bulk Vessels Index Down 10% Despite Freight Rate Rebound

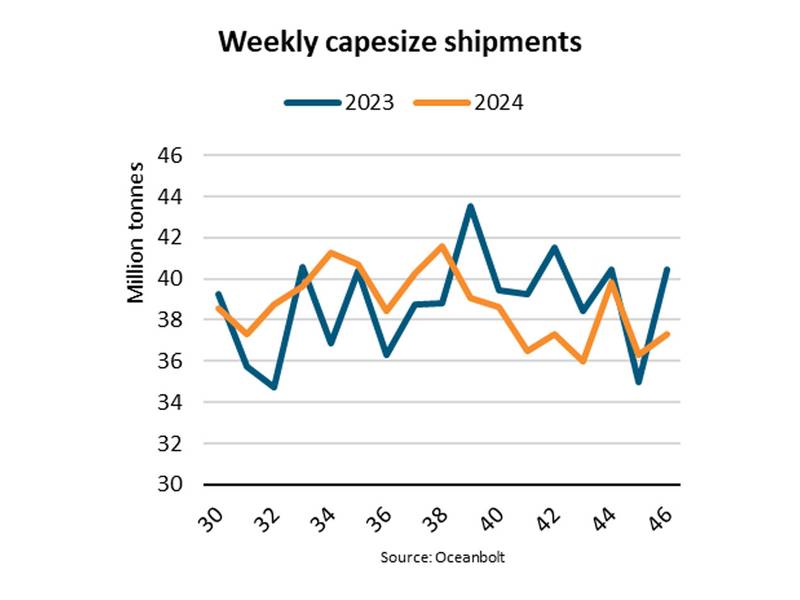

“The Baltic Dry Index (BDI) has recovered since the start of November due to stronger capesize freight rates, but the index is still down 10% y/y. The capesize market has benefited from a 1% increase in shipments so far in November compared to October 2024 and November 2023. However, the increase has not been enough to recover to the highs seen during the first three quarters of 2024,” says Filipe Gouveia, Shipping Analyst at BIMCO.

On November 19, 2024, the BDI reached 1,627 points, up from 1,374 on 4 November. Before then, the index had gradually fallen since the end of September due to weaker capesize shipments. The capesize segment accounts for 40% of the BDI and therefore, changes in this market significantly impact the index.

Currently, the BDI is down 10% y/y despite a 4% y/y increase in the Baltic Capesize Index (BCI), as other segments continue to underperform. The BDI and BCI indices were much stronger during the first three quarters of 2024 when they rose by 41% y/y and 94% y/y respectively.

“This weakening in capesize spot rates has negatively impacted market sentiment. Since the start of October, one year time charter rates have fallen by 7%, while prices for five-year-old second hand capesizes have decreased by 2%,” says Gouveia.

So far in November, capesize demand is up 4% y/y, which is notably slower than the 7% y/y growth during the first three quarters of 2024. Demand is growing faster than shipments due to longer average sailing distances. Brazilian iron ore and Guinean bauxite shipments have both risen, resulting in longer distances than for Australian cargoes.

However, while the capesize market is not as strong as it was during the first three quarters of 2024, it is still stronger than in November 2023. The supply/demand balance has marginally tightened as supply only grew by 3% y/y. The segment has benefited from low deliveries, keeping supply down even as congestion eased.

Forward Freight Agreements (FFAs) for the Baltic Exchange's Capesize 5TC indicate that the market expects rates to remain around current levels in December. During the first quarter of 2025, FFAs point to a drop in rates due to seasonality, and well below the levels seen in the first quarter of 2024.

“Looking ahead, capesize freight rates could still reach the highs of this year in 2025 as the market will likely remain strong. We currently expect the supply/demand balance in the capesize market to remain balanced with both demand and supply growing by 0.5-1.5%,” says Gouveia.

Related News