CO2 Shipping on the Rise

The transportation of CO2 is taking to the seas as emitters look for flexible ways to move captured carbon to offshore storage projects, with a fleet of 55 carriers required by 2030, according to Rystad Energy research.

Based on planned carbon capture projects, Rystad predicts that more than 90 million tonnes per annum (tpa) of CO2 will be shipped by the end of the decade, volumes requiring 48 terminals to handle the import and export of the gas.

As the global carbon capture, utilization and storage (CCUS) market expands, a significant hurdle in the value chain is the lack of available transportation and storage networks for projects. Onshore pipelines are the most common mode currently, with 330 expected to be operational by 2030. These pipelines are ideal for transporting large quantities of CO2 to onshore storage sites or coastal terminals.

Offshore pipelines are larger, transport captured carbon to underwater storage sites and are expected to play a vital role in the supply chain in the coming years. CO2 shipping is the third piece of the puzzle and the most flexible solution for carrying carbon emissions over long distances at a relatively low cost.

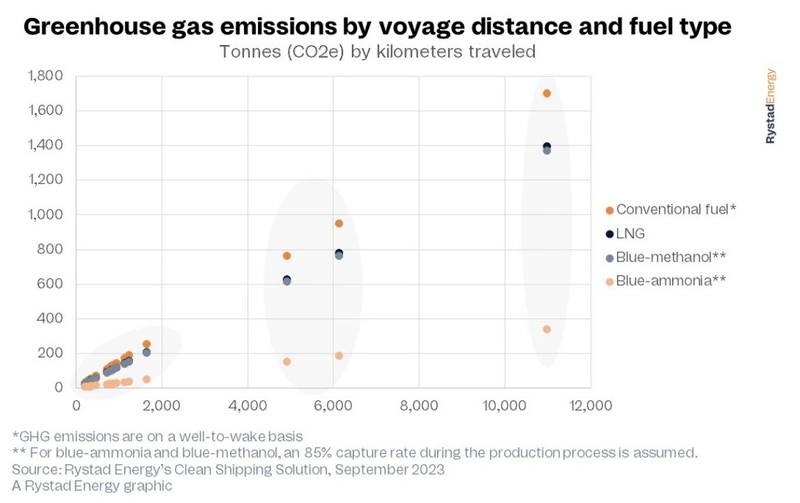

Yet, the shipping industry relies on emissions-heavy conventional fuels like maritime diesel or low-sulfur fuel oil (LSFO), calling into question the environmental impact of the process. The greenhouse gas (GHG) emissions over shorter distances may be relatively low, but the impact multiplies quickly over longer journeys.

Rystad research of CO2 shipping routes that could come online in 2030 indicates that ships traveling long distances could emit as much as 5% of the total CO2 shipped. Switching to LNG as the shipping fuel could cut emissions by 18%, while blue methanol would result in a 20% drop. The real reduction would come with the use of blue ammonia, which would slash the emissions impact of the shipping process by up to 80%.

GHG emissions for marine fuels are calculated well-to-wake, including associated emissions in the fuel's upstream production, refining and end use. Emission estimates are based on a vessel with a 25,000 cubic meter capacity.

The myriad challenges and uncertainties, including high costs, across the CCUS value chain often dissuade plant owners from exploring carbon capture opportunities. Fortunately, emerging initiatives, including the development of open-source CO2 storage infrastructure and the expansion and diversification of transportation networks, should ease some of these restraints and reduce the complexity of projects.

The North Sea is set to take center stage in the CO2 shipping surge due to its proximity to major populated areas in Northern Europe. Norway looks set to account for about 30% of all shipped carbon dioxide globally in 2030 with 26 million tpa, based on announced projects and memoranda of understanding (MOUs) – although this hinges on whether storage sites can be developed quickly enough.

The Netherlands follows Norway, with 23 million tpa, and the UK, with about 20 million tpa of forecast shipping volumes. These totals include the shipping of domestically captured CO2 plus imports from other countries. For instance, the UK has prolific subsurface storage potential and an ambitious CO2 storage target, so it will likely prioritize storing its emissions rather than shipping to its North Sea neighbors.

France is expected to ship 17 million tpa of CO2 in 2030, followed by Belgium at 13 million tpa. These countries do not have ample opportunities to store their CO2 emissions domestically, so the chance to ship CO2 to neighboring European countries will help fast-track CCUS developments.

The Northern Lights Project in Norway is set to be the first open-source CO2 transport and storage network when it opens in early 2025. The project will receive domestically shipped CO2 and volumes from northwest Europe at its onshore terminal before piping and storing the gas under the seabed. Phase one of the project will store up to 1.5 million tpa of CO2. This looks set to be the first of many such projects, each with nuances, but all will involve receiving shipped CO2 to store underground.

Australia will also be a significant player in the global market, shipping and storing CO2 from domestic projects and neighboring Asia-Pacific countries, including Japan.

Most of the proposed shipping routes – including those in Europe and around Australia – are no more than 2,500km, a relatively short journey. However, planned routes between Japan, Malaysia and Australia would involve sailing more than 5,000km. The longest journey announced to date would be between South Korea and Saudi Arabia, a one-way trip of at least 12,000km.